If you have worked for a tech startup, you have probably earned incentive stock options (ISOs) as part of your compensation. ISOs are notoriously difficult to understand, let alone to strategize. In most cases, it frankly doesn’t matter, because most startups will not become spectacularly successful, and therefore, the options will never become a dominant part of the money you made during your stint. But, if you are lucky enough to hitch a ride on a unicorn 🦄, it can get very complicated, indeed.

The tax treatment of ISOs encourages employees to take financial risks, in return for potential tax advantages. If there were no tax advantages to be gained, it would be advantageous in all cases to exercise options as late as possible—either just before expiration or when you want to sell the stock—because you would have maximal certainty of the value of the shares. But because there are holding periods for tax advantages and triggers for taxable events, there is pressure to exercise earlier. This means locking up cash for years, before knowing when, or even if, the shares can be sold for profit.

The one thing you must understand about ISOs is the concept of a qualifying disposition. I’m going to first explain what that means, and then present a brief case study from my own situation.

I have tried to understand employee equity for the better part of the past decade, starting with my experience cofounding a startup. There are many explainers out there on the ins and outs of stock options, early exercising, and 83(b) elections. There are also many armchair experts (like myself). I must warn you that I have concluded that most of us are wrong 1. I continue to learn things that force me to reevaluate my understanding. After all this time, I have literally only in the past week come to understand what I’m sharing here 2. So take this with a huuuge grain of salt, read the references yourself, and confirm your understanding with a professional. Then, ask that professional to help you plan your exercise strategy. If you find yourself in a situation where you have a life changing amount of equity, it’s worth it to get it right.

ISOs are tricky because they have different tax treatment under the regular and alternative minimum tax (AMT) codes, and they also have completely different tax treatment depending on the timing of when you sell them. The AMT part is better known. The nuances of the timing part are not. I’m going to skip over the basics of stock options here and assume that you know the definitions of share, option, exercise price, fair market value, and bargain element 3. Those are adequately explained many places. What is not typically adequately explained is the tax treatment.

The basics

The key benefit of ISOs is that they can have some tax advantages, in terms of sometimes delaying when taxes are due 4 and enabling favorable long-term capital gains treatment (LTCG). Specifically, they can be advantageous if you exercise your options at a time when the fair market value (FMV) is greater than the exercise price. This might happen if you join a startup on a strong growth trajectory. With normal options, exercising would be a taxable event in the year the options are exercised, and you would pay income taxes on the bargain element.

The tax situation at the time of sale of an ISO is very different depending on whether that sale is considered a qualifying disposition or not. To be a qualifying disposition, the sale of the share must be both 2 years after the option grant date and 1 year after exercise 5. If these two requirements are met, the difference between the exercise price and the sale price is treated as a long-term capital gain. Easy peasy 6. Major tax savings.

However, if the holding period is not met before selling, the sale is considered a disqualifying disposition 😱, and it’s almost as though the option loses its special ISO treatment and becomes mostly as though it had been an NSO:

- The bargain element—the difference between the exercise price and the FMV at the time of exercise—is now taxed as ordinary income. This income realized in the year that the share was sold, instead of the year in which it was exercised (because, at the time of exercise, no one knows the future to say whether you will meet the qualifying disposition requirements at the time of sale).

- Normal capital gains rules apply to any further gains. If the shares were held for a year, they are long-term capital gains. Otherwise, they are short-term capital gains and taxed as income.

Early exercise gets squirrely

Early exercising is buying shares from options that haven’t yet vested. When combined with 83(b) election, it is a strategy designed to lock in a low bargain element and start the holding periods for long-term capital gains. But, importantly, the effect of early exercising on capital gains treatment of the bargain element also appears to be dependent on whether the disposition is qualifying or disqualifying and whether an 83(b) election was made. In the case of a qualifying disposition, the 1-year holding period begins at the time of exercise 5. In the case of a disqualifying disposition, the 1-year holding period begins once the share vests 7.

Also, it seems that the 83(b) election is not applicable to ordinary income tax, in the case of a disqualifying disposition. Normally, the purpose of the 83(b) election is to lock in the bargain element to the time of an early exercise, instead of letting it be determined in the future, when the shares vest. If stock is sold in a disqualifying disposition, the bargain element of each share (and thus, compensation taxable as ordinary income) will be the spread between the exercise price and the FMV on the vest date of that share ‼. If there are further gains between the vest date and the sale date, those will be treated as short- or long-term capital gains, whichever is appropriate. However, the 83(b) election will be applicable for AMT purposes 🤷♂️ 8.

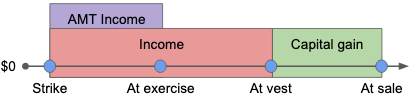

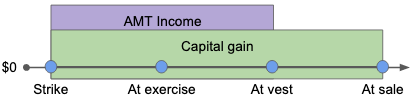

This is probably hard to understand, so I’ve tried to summarize these scenarios. These assume an increasing share value. It’s common for some of these values to be the same. For instance, one might exercise while the FMV is the same as the exercise price, to avoid realizing AMT-taxable income. If a company has down times, it’s also possible for the value to decrease. AMT is realized in the year of exercise; the other taxes are realized in the year of sale.

| Qualifying disposition? | |||

| Yes | No | ||

| 83(b) election? | Yes |

The entire spread between exercise price and sale price is considered a capital gain. The LTCG holding period was accelerated by the 83(b) election, and is therefore already satisfied. AMT income in the year of exercise is calculated from the bargain element at the time of exercise.  |

Spread between value at time of vest and exercise price treated as income (83(b) election is nullified for this). Additional gain beyond value at time of exercise is a capital gain; hold for 1 year from vesting for LTCG. AMT income in the year of exercise is calculated from the bargain element at the time of exercise.  |

| No |

Entire spread between exercise price and sale price treated as a capital gain; hold 1 year from vesting for LTCG. AMT income in the year of exercise is calculated from the bargain element at the time of vesting. 9  |

Spread between value at time of vest and exercise price treated as income. Additional gain beyond value at time of exercise is a capital gain; hold for 1 year from vesting for LTCG. AMT income in the year of exercise is calculated from the bargain element at the time of vesting.  |

|

Why does this matter?

I’m sure this all seems very niche, but I’m writing about this because it was relevant to my situation. I’ll try to present it in simplified form:

I have an ISO grant from 1/10/20. On Day 1, I couldn’t afford to early exercise my entire grant and claim 83(b) election. But I did want to get holding periods going for long-term capital gains treatment for at least some of my shares and avoid potential AMT events in the future, so I decided to exercise in stages. One of my exercises was on 1/14/21, and it included some unvested shares, which would vest on 4/8/21. By April, the FMV had increased from what it had been on the exercise date. Like, very substantially. Good thing I had filed that 83(b) election, or I would have set myself up for a big AMT bill, due in 2022.

I wanted to figure out when exactly I’ll be able to sell my shares without losing tax benefits. It was clear to me that if I sell my shares before 1/14/22, I’ll definitely have to pay ordinary income tax on the gains. But I was trying to figure out, if I decide to sell on 1/14/22, would they have long-term capital gains treatment, or would I have to wait until 4/8/22 for those shares to hit one year from their vest date? Applying the reasoning above, it seems that do have the option to sell on 1/14/22 for the best tax treatment.

In conclusion

If you are able to meet the requirements of a qualifying disposition, ISOs have great tax advantages. But, as this piece points out, this comes at the cost of being subject to a holding period of 2 years from grant, the complexity of AMT, and potentially worse treatment than NSOs if you make a disqualifying disposition of early exercised shares. Hope this helps, and may the odds of the startup lottery 📈 be ever in your favor.

Special thanks to the many people who have read drafts of this post. I’ve run it by a few experts, but they cannot be cited, for compliance reasons. Again, review this info with an expert before making any of your own financial decisions.

1 I’ve seen enough misconceptions that I question whether anybody actually gets this right when they file taxes. Maybe the IRS barely does any follow-up? Maybe the software just does the right thing? If you read through the laws and regs, it’s clear that the answers to seemingly simple questions require pulling info from several places. In any case, I don’t think it’s possible to explain this topic correctly without using the words “qualifying disposition”, and the rest of this piece shows why.

2 For this, I am indebted to the this piece by Joshua Levy and Joe Wallin, this piece by Robert W. Wood and Jonathan R. Flora, and the advice of the CFPs my family works with.

3 Okay, fine, I’ll explain bargain element. It’s the difference in the exercise price of the option (which is fixed) and the fair market value at the time of exercise (which typically changes). Generally, if you receive property (like a share of stock) from your employer that is worth more than you paid for it, then the difference is considered taxable income. The rules around ISOs create an exception to this principle.

4 “Sometimes” because the AMT makes sure that the government gets an early crack at your bargain element gains, if they are significant. My understanding is that you may get to credit this against your future taxes, but this is something I haven’t studied in depth. This explainer may be helpful.

5 Exercising the option constitutes a transfer, according to CFR 1.421-1(g), and the holding period rules are outlined in CFR 1.422-1(a). CFR 1.83-4(a) confirms that By the way, the Code of Federal Regulations (CFR) contains all of the rules made by the Executive Branch to implement the laws passed by Congress, which are generally written to allow some interpretation. For the purposes of this topic, these are the rules the IRS has written that define and explain the tax treatment of ISOs.

6 Well, aside from AMT.

7 As confusing as this is, it is explicitly outlined in Example 2 of CFR 1.422-1(b)(3).

8 CFR 1.421-2(b), on disqualifying dispositions, explains that the treatment of stock will be as described in CFR 1.83-1(a)(1), and the holding period begins at vest, as described in CFR 1.83-4(a).

9 As far as I can tell, there’s no reason to early exercise ISOs and not elect 83(b). One could say it would be useful if you have decided you want to exercise some upcoming options and you don’t want to bother exercising every time you vest. But it exposes you to the uncertainty of the FMV at the future vest date, which cannot be worth the convenience. If you don’t file an 83(b), every vesting day of your early exercised shares is an AMT-taxable event. This case is still useful to cover, because many people fail to correctly file their 83(b) election.